A Deep Dive Into the Class Action Settlement Finder: How the Technology Works, What It Actually Recovers, and Whether It’s Right for You

Primary keyword: money pilot reviews

If you have ever gotten an email that starts with “You may be a member of a class action lawsuit” and then immediately archived it because the form looked too complicated, you are not alone. Research cited on MoneyPilot’s own blog estimates that 91% of eligible claimants never file for the class action settlements they qualify for. That is not because the money is not real. It is because the process is fragmented, easy to forget, and often hidden behind administrative friction that exhausts most people before they finish.

In 2025 alone, more than $70 billion in class action settlements were paid out, with over 13,000 class actions filed. A lot of that money goes unclaimed. If you have ever shopped on Amazon, streamed Netflix, used a major bank, bought electronics, or had data involved in a breach (which is, practically speaking, everyone), there is a reasonable chance you have qualified for at least one settlement in the past several years without realizing it.

MoneyPilot exists because that gap between “eligible” and “actually receiving the check” is enormous, and the company is betting that most people would rather pay a subscription fee to have the whole process handled for them than spend hours each week hunting down settlement portals, filling out claim forms, and tracking deadlines across dozens of cases.

This review will walk through exactly how the technology works, what it can and cannot do, what users are reporting, and the specific questions you should ask yourself before deciding if it is worth the subscription.

What Is MoneyPilot?

MoneyPilot is a financial recovery platform operating at moneypilot.com and as an iOS app. Its core function is to help users discover class action settlements they qualify for, file claims on their behalf, and track payouts through completion. Beyond settlements, the platform also scans for forgotten subscriptions, flags unusual recurring charges, and provides basic spending insights.

The service operates on a subscription model with monthly, quarterly, and 6-month plans. It is important to be upfront about this: MoneyPilot is not a free tool. You are paying for automation and convenience, not for access to settlement information itself (which is technically public). The value proposition is whether the time saved and the settlements actually recovered exceed what you pay in subscription fees.

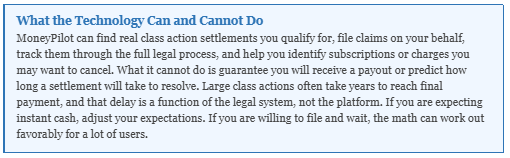

The company explicitly states that it does not guarantee payouts, does not act as a law firm, and does not make eligibility decisions. All claim approvals and payments are handled by courts and official settlement administrators. MoneyPilot’s role is strictly in the discovery, filing, and tracking layer.

How the Technology Actually Works

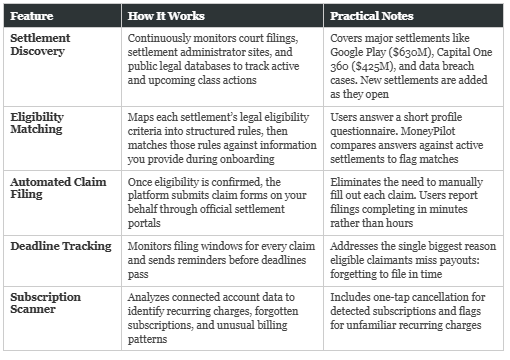

Let us walk through what MoneyPilot does under the hood, because the actual process is more interesting than the marketing language suggests. The platform is built on five interconnected stages, each addressing a specific aspect of the settlement recovery problem.

Stage 1: Continuous Settlement Monitoring

The foundation of MoneyPilot is a monitoring system that tracks active and upcoming class-action settlements across multiple public sources. This includes court filings, settlement administrator websites, legal news databases, and federal court dockets. New settlements are added as they open, and the system automatically flags filing deadlines.

This is the same kind of data aggregation that legal research firms and consumer protection organizations do, just packaged for individual consumers rather than corporate clients. The data itself is public. What MoneyPilot adds is the infrastructure to process it at scale and keep it current.

Stage 2: Eligibility Rule Mapping

Every class action settlement has its own eligibility criteria. Some require you to have purchased a specific product between certain dates. Others require you to have been a customer of a particular bank. Others require you to have had personal data compromised in a specific breach. These rules are typically written in dense legal language that most people cannot parse.

MoneyPilot’s system converts these legal eligibility requirements into structured, machine-readable rules. When you complete the onboarding questionnaire (which takes about two minutes), your answers are cross-referenced against those rules to identify every settlement you likely qualify for. This is where the real technical value sits: translating hundreds of legal documents into a single matching engine.

Stage 3: Automated Claim Filing

Once eligibility is confirmed, MoneyPilot files the claim on your behalf. This is the step that saves the most time. Filing a single settlement claim manually can involve finding the right portal, creating an account, entering personal information, uploading documents if required, and confirming submission. Multiply that by 5 or 10 settlements and you have lost an afternoon.

MoneyPilot automates this by maintaining integrations with settlement claim portals and submitting the required information programmatically. Users report filing claims for multiple settlements within minutes rather than hours. One Trustpilot reviewer described it as “literally 2 minutes per claim.”

Stage 4: Deadline and Status Tracking

Class action settlements often have filing windows measured in months, and payouts can take years after a claim is approved. This is where most people drop the ball: they file a claim, forget about it, and never follow up when the check eventually arrives or when additional documentation is requested.

MoneyPilot tracks the status of every claim through the full lifecycle: filed, under review, approved, paid. It also sends reminders before deadlines pass for settlements you have not yet claimed. Multiple users in the recent Trustpilot reviews specifically credited this feature with catching claims they would have otherwise missed.

Stage 5: Subscription and Charge Monitoring

The less-advertised but arguably equally valuable part of MoneyPilot is the subscription scanner. After connecting your financial accounts, the platform identifies recurring charges and forgotten subscriptions, flags unusual billing patterns, and offers one-tap cancellation for detected subscriptions.

This is a legitimate category of financial tool that has existed separately for years (services like Rocket Money and Truebill built entire businesses around just this feature). MoneyPilot’s move is to bundle it with the settlement finder, which makes some intuitive sense since both are about recovering money you did not know you were losing.

What Users Are Actually Reporting

As of this review, MoneyPilot has a 2.3/5 rating on Trustpilot across 39 reviews. That number alone does not tell the whole story. The distribution is heavily polarized: 28% of reviews are 5-star, 72% are 1-star, and there are essentially no reviews in the middle. This is a pattern worth understanding because it reflects two different groups of users having very different experiences with the same product.

The Positive Reports

The 5-star reviews cluster around a consistent set of themes: settlements recovered that users did not know about, ease of use, and a reliable reminder system. A sample of what recent users have said includes:

Jerry (AU, February 2026, 5 stars): was impressed by how effortless the process was and reported recovering a few hundred dollars from settlements they had no idea were pending, noting that each claim took about 2 minutes.

Hsiisojsi Roaktai (ES, February 2026, 5 stars): said they had been looking for something like MoneyPilot for years and reported finding $290 from old Netflix and Amazon settlements.

Lisa Parker (US, February 2026, 5 stars): said MoneyPilot showed her 8 settlements she qualified for based on the onboarding quiz, and that she had already filed for 4 of them with no proof of purchase required.

Tom Henderson (US, February 2026, 5 stars): described being skeptical initially but filed $380 in claims within days after connecting accounts, and confirmed receiving his first check.

Hannah Collins (GB, February 2026, 5 stars): credited MoneyPilot’s reminder system for getting her to actually submit a claim she would have otherwise skipped.

The consistent thread in these reports is that users found real settlements, completed real filings, and in several cases have already received real checks. That is what the product is designed to do, and when it works, it works as advertised.

The Critical Reports

The 1-star reviews cluster around a different set of issues, most of which are about the subscription model rather than the settlement technology itself. The most common complaint is frustration with recurring charges, difficulty canceling, or feeling that the subscription was not clearly disclosed at signup. Some users report filing claims but waiting longer than expected for payouts, which is a legitimate frustration but reflects how class action settlements actually work (court-approved payouts often take 12 to 24 months or longer).

One pattern worth noting is that some of the critical reviews describe situations where users did not realize they had enrolled in a recurring subscription rather than a one-time purchase. This is a real issue and one the company has publicly acknowledged by responding to 96% of negative reviews on Trustpilot, typically within 48 hours.

The Brand’s Recent Improvements

Looking at the recent review activity on Trustpilot, there is a clear shift happening. The 5-star reviews in the dataset are concentrated in February and April 2026, and they consistently describe positive experiences with both the product and the company’s responsiveness. The company is also visibly engaging with negative reviews, offering refunds and resolution paths publicly on the Trustpilot page.

A few things stand out in the recent activity: MoneyPilot has a Paid Trustpilot subscription and a Claimed Profile, meaning they are officially managing their presence on the platform and responding to customer feedback rather than letting it sit unaddressed. The response rate of 96% to negative reviews within 48 hours is a meaningful operational commitment. Users who have had billing issues in recent months are being directed to support channels that appear to be working, based on the absence of follow-up complaints from the same reviewers.

None of this erases the earlier frustrations that drove the 1-star reviews, but it does suggest a company that is actively working to fix the issues rather than ignoring them. For someone evaluating MoneyPilot today, the question is less about what happened six months ago and more about whether the current experience is trending in the right direction. Based on recent reviews, it appears to be.

Is MoneyPilot Worth It? Doing the Math

This is the core question, so let us actually work through it. MoneyPilot is a subscription service, so the value calculation is straightforward: does the amount of money you recover exceed the amount of money you pay in subscription fees?

Based on user reports, MoneyPilot typically surfaces between $200 and $640 in eligible settlements per user during the initial onboarding process. Some users report higher amounts, particularly those with years of shopping history across major retailers and banks. The subscription cost is significantly lower than these recovery amounts, meaning that for most users who actually complete the filings, the math works out favorably even in the first month.

There are three scenarios where MoneyPilot makes the most sense:

You have significant consumer history. If you have been shopping online, using major banks, streaming services, or had any data involved in breaches over the past several years, you likely qualify for multiple settlements right now. The more active your consumer footprint, the higher the expected recovery.

You value time over DIY effort. You could find and file all of these settlements manually using free resources like TopClassActions.com. If you are the kind of person who will actually sit down, search weekly, and fill out claim forms for each one, you do not need MoneyPilot. Most people are not, which is why 91% of eligible claimants never file.

You also want subscription management. If you are paying for MoneyPilot primarily for the settlement finder, the subscription scanner is a meaningful bonus. Standalone subscription managers like Rocket Money cost similar amounts for just that feature, so bundling gets you two tools for the price of one.

There are also scenarios where MoneyPilot may not be the right fit:

You have minimal online shopping or banking history. If your consumer footprint is small, the number of settlements you qualify for will be small, and the math may not work in your favor.

You are uncomfortable with subscription services generally. If recurring charges make you anxious or you have had bad experiences with subscription management in the past, consider whether the convenience is worth that tradeoff for you personally.

You need immediate cash. Class action settlements take time. If you are expecting a check this week, MoneyPilot is not the right tool. The payouts are real but they arrive on the courts’ timeline, not yours.

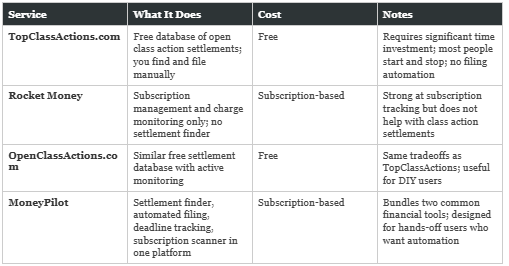

How MoneyPilot Compares to Alternatives

MoneyPilot is not the only option in this space, though the combination of settlement filing plus subscription management in one dashboard is relatively rare. Here is how it stacks up against the main alternatives.

The honest comparison is this: you can replicate most of what MoneyPilot does for free if you are willing to do the work. What you are paying for is the automation layer that turns a multi-hour process into a two-minute one. For some people that automation is worth every penny. For others it is not. That is the honest tradeoff.

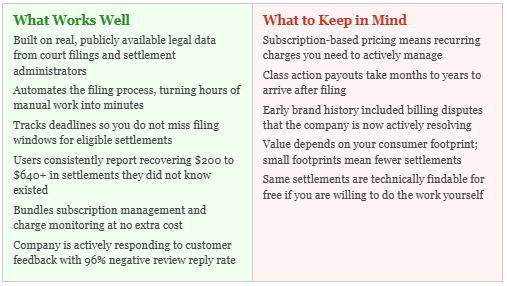

The Breakdown: What Works and What to Watch

Practical Tips if You Decide to Try It

Start with the shortest plan. If MoneyPilot offers a monthly plan, start there rather than committing to 6 months. Give the product one full billing cycle to prove its value to you before upgrading to a longer commitment.

Complete the full onboarding questionnaire. The platform can only find settlements you qualify for if it has enough information to match you against eligibility rules. Rushing through the setup will result in fewer matches.

File every claim it surfaces. Most class action settlements require minimal effort once the platform has filed the paperwork. There is no downside to filing for everything you qualify for, and you do not know which ones will actually pay out until they do.

Track your own results. Keep a simple spreadsheet of what you filed, when, and what you eventually receive. This will tell you definitively whether MoneyPilot is worth the subscription for your specific situation, which is better than relying on general averages.

Set a calendar reminder to review your subscription. Treat this like any subscription service: review it every few months and ask yourself whether you are still getting value. If yes, keep it. If not, cancel it. This applies to MoneyPilot and every other recurring service you pay for.

Be patient on payouts. Class action settlements operate on legal timelines, not consumer timelines. A settlement you file for today might not pay out for 12 to 24 months. That is not MoneyPilot’s fault; it is how the court system works.

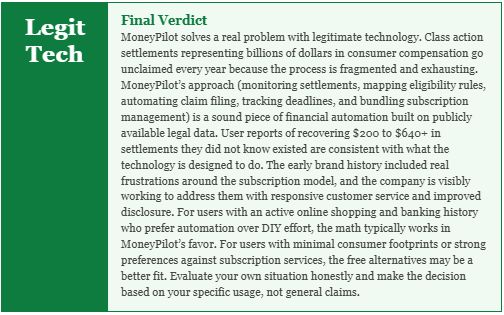

The Bottom Line

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. MoneyPilot does not guarantee settlement payouts, and eligibility is determined by courts and settlement administrators. Class action payouts are subject to court schedules and can take extended periods to resolve. Individual results vary based on consumer history and the specific settlements available at the time of filing. This review is based on publicly available user reviews, company documentation, and publicly reported information as of April 2026.